Facing care home costs averaging £52,000 to £78,000 per year can feel overwhelming—particularly when you're already exhausted from months or years of caring, worried about your parent's deteriorating health, and trying to navigate a system that often feels like it's working against you rather than for you.

Here's something that might surprise you: research shows that only 14% of UK families are aware of NHS Continuing Healthcare (CHC)—a scheme that could provide fully funded care worth up to £76,000 per year. Thousands of eligible families are paying unnecessarily, simply because they don't know this option exists or how to access it.

Understanding care home funding eligibility isn't just about saving money. It's about accessing the care your loved one deserves without the financial hardship of depleting a lifetime of savings, selling the family home, or sacrificing your own financial security.

This guide explains the three main funding pathways in England, who genuinely qualifies for each, and how to navigate a complex system with greater confidence—based on real experiences from families who've been through it.

A note before we begin: If you're reading this whilst juggling caring responsibilities, dealing with hospital discharge pressure, or simply exhausted from trying to understand conflicting information—you're not alone. Families consistently describe the UK care funding system as confusing, frustrating, and at times feeling deliberately obstructive. This is genuinely difficult, and it's not your fault if you find it overwhelming. What follows is clear, honest information to help you make informed decisions without the confusion.

Last updated: January 2026.

Quick Start: Am I Eligible for Funding? (5-Minute Assessment)

Answer these 5 questions to identify your most likely funding pathway:

Question 1: Health Needs Assessment

Does your loved one have 3 or more of these at a severe level?

- [ ] Complex medical interventions (PEG feeding, tracheostomy, IV meds, catheter management)

- [ ] Severe immobility (requires 2+ person transfers, specialist equipment)

- [ ] Advanced dementia with severe behavioral challenges (aggression, constant supervision)

- [ ] Grade 3-4 pressure ulcers or complex wound care

- [ ] Frequent seizures or altered consciousness requiring monitoring

- [ ] Severe respiratory needs (oxygen 24/7, suctioning, ventilation)

- [ ] Severe swallowing difficulties with aspiration risk

If YES to 3+: ➡️ NHS CHC likely - Request Checklist assessment immediately If NO: ➡️ Continue to Question 2

Question 2: Financial Assets Assessment

What is your total capital (savings + investments + property value if counted)?

- [ ] Under £14,250: Maximum LA support - you pay from income only

- [ ] £14,250 - £23,250: Partial LA support - tariff income applies

- [ ] £23,250 - £100,000: Self-funder BUT may qualify for DPA if property is main asset

- [ ] Over £100,000: Self-funder - explore DPA or self-pay

Result: Identifies your means test band

Question 3: Property Situation

Does your property situation qualify for disregard?

- [ ] Spouse/partner lives in property: Property fully disregarded ✅

- [ ] Qualifying relative lives there (60+, under 16, disabled): Disregarded ✅

- [ ] Been in care less than 12 weeks: Temporary disregard ✅

- [ ] Property empty, been in care 12+ weeks: Property counted ❌

- [ ] Renting out property: Property counted + rental income assessed ❌

Result: Determines if property affects means test

Question 4: Urgency Level

What is your timeline?

- [ ] Planning ahead (not yet in care): Time to prepare, apply for CHC, organize finances

- [ ] Hospital discharge imminent (48-72 hours): Request CHC Checklist, contact council urgently

- [ ] Already in care home, self-funding: Apply for retrospective CHC if needs changed, monitor capital depletion

- [ ] Crisis situation (unsafe at home): Emergency care needs assessment, immediate CHC request

Result: Determines your action timeline

Question 5: Primary Health Need Test

Is your loved one's care need primarily health-related rather than social care?

Health-related needs (points toward CHC):

- Registered nurse interventions required daily

- Complex drug regimes needing specialist monitoring

- Medical equipment management (ventilator, feeding pump)

- Unpredictable health crises requiring constant clinical monitoring

Social care needs (points toward LA funding):

- Help with washing, dressing, meals (personal care)

- Supervision and companionship

- Help with mobility (not complex medical)

- Memory support and reminders

If primarily health-related: ➡️ CHC pathway - strong case If primarily social care: ➡️ LA means test pathway

Your Quick Assessment Result

Path A: NHS CHC Strong Candidate

If:

- Question 1: YES to 3+ severe health needs

- Question 5: Primarily health-related

Action:

- Request CHC Checklist immediately (from hospital, GP, or care home)

- Gather medical evidence (see document checklist later)

- Don't wait - apply regardless of financial position

- If approved: 100% of care costs funded by the NHS

Path B: Local Authority Funding

If:

- Question 1: NO (limited health needs)

- Question 2: Capital under £23,250

- Question 5: Primarily social care needs

Action:

- Contact council social services for Care Act assessment

- Prepare financial documents (bank statements, property valuation)

- Understand your contribution based on means test

- Council contribution depends on your means test result

Path C: Deferred Payment Agreement (DPA)

If:

- Question 1: NO (CHC unlikely)

- Question 2: Capital over £23,250 (mainly property equity)

- Question 3: Property counted (not disregarded)

Action:

- Apply for DPA with local council within 12-week disregard period

- Avoid rushed house sale

- Understand interest costs (4.69% per year)

- Benefit: Defer sale until after lifetime, preserve choice

Path D: Self-Funding with CHC Application

If:

- Question 1: BORDERLINE (some severe needs but unclear)

- Question 2: Capital over £23,250

- Question 4: Already in care, paying privately

Action:

- Apply for CHC assessment anyway (not means-tested)

- Keep detailed records of all care costs and health interventions

- If approved later, claim retrospective refund

- If approved later, you may be eligible for retrospective funding of care costs already paid

Use our Eligibility Assessment Tool for detailed analysis →

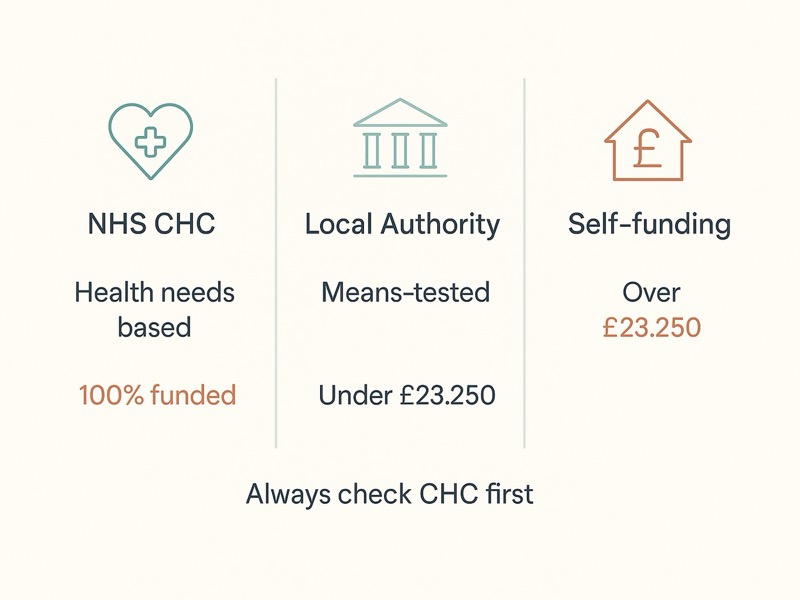

Understanding the UK Care Funding Landscape

Before diving into eligibility criteria, it's crucial to understand that care home funding in England operates through three distinct pathways:

1. NHS Continuing Healthcare (CHC)

- What it covers: 100% of care home fees, including accommodation

- Who it's for: People with significant, ongoing healthcare needs

- Eligibility: Based on health needs assessment, not financial circumstances

- Annual value: Up to £76,000 per year (fully funded)

2. Local Authority (Council) Funding

- What it covers: Partial or full funding, depending on means test

- Who it's for: People with care needs who have limited financial resources

- Eligibility: Based on capital assets and income thresholds

- What you pay: Depends on your savings and income

3. Self-Funding (Private Pay)

- What it covers: You pay the full care home fees

- Who it's for: People with assets above £23,250

- Options: May include Deferred Payment Agreements to protect your home

The critical question is: which pathway applies to you?

Quick Comparison: The Three Funding Pathways

| Criteria | NHS Continuing Healthcare (CHC) | Local Authority (Council) Funding | Self-Funding (Private Pay) |

|---|---|---|---|

| Who qualifies | Those with significant, complex healthcare needs | Those with capital under £23,250 | Those with capital over £23,250 |

| Based on | Health needs assessment (12 care domains) | Financial means test (assets + income) | Personal choice/no other option |

| Who pays | NHS pays 100% of all fees | Council pays most/all, you contribute from income | You pay all fees yourself |

| Annual cost to you | £0 (fully funded) | £0 - £20,000+ (varies by income) | £52,000 - £78,000+ |

| Property considered? | No - not means tested | Yes, unless spouse/qualifying relative lives there | N/A - you're paying regardless |

| Application process | CHC Checklist → Full DST assessment | Financial assessment by council | Direct arrangement with care home |

| Typical timeline | 28 days - 3 months | 2-6 weeks | Immediate |

| Success rate | ~40% approved initially, more on appeal | Depends on finances (automatic if eligible) | 100% (no eligibility barrier) |

| Can you appeal? | Yes - local resolution, ICB, IRP | Yes - for incorrect assessments | N/A |

| Annual value if approved | Up to £76,000/year (fully funded) | Varies by means test result | None |

Key takeaway: Always explore CHC first, regardless of financial position. Even wealthy families can access 100% NHS funding if health needs qualify. Only if CHC is rejected should you consider the means-tested LA route or self-funding options like Deferred Payment Agreements.

NHS Continuing Healthcare Eligibility: The £76,000 Question

NHS Continuing Healthcare is often called "the best-kept secret" in UK care funding. Despite being a legal entitlement, awareness is low — many eligible families don't know about it, meaning they may be paying for care the NHS should cover.

What is NHS Continuing Healthcare?

CHC is fully funded NHS care for people who have been assessed as having a "primary health need." This isn't about having a specific diagnosis—it's about the nature, complexity, intensity, and unpredictability of your healthcare requirements.

The 12 Care Domains: Your CHC Eligibility Framework

NHS Continuing Healthcare eligibility is determined using the Decision Support Tool (DST), which assesses needs across 12 care domains. Each domain is rated from "no need" to "priority" level:

1. Breathing

What's assessed: Respiratory support requirements, oxygen dependency, ventilation needs Indicators of higher eligibility: Requires suctioning, tracheostomy care, ventilator support, frequent interventions

2. Nutrition (Food and Drink)

What's assessed: Ability to eat and drink safely, nutritional status Indicators of higher eligibility: PEG feeding, NG tube, severe dysphagia, aspiration risk requiring constant monitoring

3. Continence

What's assessed: Bladder and bowel management needs Indicators of higher eligibility: Indwelling catheter, stoma care, severe incontinence with skin integrity issues, requires 2+ person assistance

4. Skin Integrity (Including Tissue Viability)

What's assessed: Pressure sores, wounds, skin breakdown risk Indicators of higher eligibility: Grade 3-4 pressure ulcers, extensive wound care, complex dressings requiring specialist input

5. Mobility

What's assessed: Ability to move, transfer, reposition Indicators of higher eligibility: Completely immobile, requires 2+ person transfers, specialist equipment, frequent repositioning (2-hourly)

6. Communication

What's assessed: Ability to understand and be understood Indicators of higher eligibility: Non-verbal, requires specialist communication tools, severe dysphasia affecting all communication attempts

7. Psychological and Emotional Needs

What's assessed: Mental health conditions, anxiety, depression, emotional distress Indicators of higher eligibility: Severe mental health conditions, acute psychological distress, requires psychiatric input, self-harm risk

8. Cognition

What's assessed: Memory, understanding, decision-making capacity Indicators of higher eligibility: Severe dementia, complete loss of capacity, requires constant supervision, significant safety risks

9. Behaviour

What's assessed: Challenging behaviours, aggression, distress Indicators of higher eligibility: Physical aggression requiring restraint protocols, severe agitation, constant 1:1 supervision needed, risk to self/others

10. Drug Therapies and Medication

What's assessed: Medication complexity, side effects, monitoring requirements Indicators of higher eligibility: IV medications, multiple complex drug regimes, requires specialist monitoring, frequent adjustments

11. Altered States of Consciousness

What's assessed: Consciousness level, seizures, neurological episodes Indicators of higher eligibility: Frequent seizures requiring intervention, fluctuating consciousness, requires neurological monitoring

12. Other Significant Care Needs

What's assessed: Any other healthcare needs not covered above Indicators of higher eligibility: Multiple needs across categories, complex sensory impairments, end-of-life care needs

The "Primary Health Need" Test

Having high needs in several domains isn't enough alone. The assessment must demonstrate that your needs are primarily health-related rather than social care needs. Key indicators include:

- Nature: Are needs primarily health-related (nursing, medical interventions) vs social care (assistance with daily living)?

- Complexity: Do needs require specialist health knowledge to manage?

- Intensity: Are interventions frequent and require skilled input?

- Unpredictability: Do needs fluctuate rapidly, requiring constant monitoring?

Who Typically Qualifies for CHC?

While every case is individual, CHC eligibility is more likely when someone has:

Multiple severe needs across different domains:

- Advanced dementia PLUS challenging behaviour PLUS continence issues PLUS mobility problems

- Severe stroke with dysphagia, immobility, and catheter care

- End-stage conditions requiring palliative care and symptom management

Complex health conditions requiring specialist nursing:

- PEG feeding with aspiration risk

- Tracheostomy care

- Multiple pressure sores requiring complex wound management

- Unstable diabetes with frequent monitoring needs

- Frequent seizures requiring emergency protocols

High unpredictability:

- Rapidly deteriorating condition

- Frequent medical crises

- Behaviours that pose immediate risks

- Needs that change hour-by-hour

Common CHC Misconceptions

Myth: "You need a terminal diagnosis to qualify." Reality: While end-of-life care often qualifies, many people with chronic complex conditions also meet criteria.

Myth: "Dementia alone qualifies for CHC." Reality: Dementia itself rarely meets CHC criteria. It's the combination of dementia PLUS other complex health needs (falls, challenging behaviour, nutrition issues) that may qualify. For a detailed guide on how dementia and CHC eligibility interact, see Does Dementia Qualify for NHS Continuing Healthcare?

Myth: "If you're in a nursing home, NHS pays." Reality: Nursing homes and NHS-funded care are different. Many nursing home residents still self-fund or receive Local Authority support.

Myth: "CHC is only for elderly people." Reality: CHC is for anyone aged 18+ with qualifying health needs, including younger adults with disabilities or acquired brain injuries.

Real Scenarios: 4 Families, 4 Different Funding Outcomes

Scenario 1: Dorothy (81) - NHS CHC Approved (Saved £76,000/Year)

Background:

- Advanced vascular dementia with severe behavioral disturbances

- Grade 4 pressure ulcer requiring complex wound management

- PEG feeding due to severe dysphagia (aspiration risk)

- Requires 2-person transfers, completely immobile

- Frequent UTIs requiring IV antibiotics

- Episodes of severe agitation, attempted self-harm

Financial situation:

- Savings: £45,000

- Property: £280,000 (no one living there)

- State pension: £230/week

- Family initially thought they'd have to sell house

CHC Assessment Scores:

- Breathing: Moderate

- Nutrition: Severe (PEG feeding, aspiration risk)

- Continence: High (catheter, frequent UTIs)

- Skin: Priority (Grade 4 pressure ulcer, tissue viability nurse input)

- Mobility: Severe (completely immobile, 2-person hoist)

- Cognition: Severe (advanced dementia, no capacity)

- Behaviour: High (severe agitation, self-harm risk, 1:1 supervision)

- Drug therapies: High (complex regime, IV antibiotics)

Outcome: ✅ CHC APPROVED after 10-week assessment

- NHS pays 100% of care home fees (£1,460/week = £75,920/year)

- Property not considered (CHC not means-tested)

- Family kept savings and house

- Dorothy received specialist nursing care in nursing home

Key lesson: Multiple severe needs across domains = strong CHC case. Even with £325,000 in assets, family paid £0 because health needs qualified.

Scenario 2: Robert (76) - CHC Rejected, Successful Appeal (18-Month Fight)

Background:

- Severe COPD requiring oxygen 24/7

- Type 2 diabetes with neuropathy

- Multiple pressure sores (Grade 2-3)

- Confusion and short-term memory issues

- Frequent falls, mobility severely compromised

Initial CHC Assessment: ❌ REJECTED - Decision stated needs were "primarily social care with some health needs"

Family's Challenge: Robert's daughter Sarah disagreed. She gathered:

- GP notes showing 8 hospital admissions in 12 months

- District nurse records (visiting 3x weekly for wound care)

- Care home daily notes showing oxygen adjustments, fall incidents

- Evidence of unpredictability (COPD exacerbations requiring emergency interventions)

Appeal Timeline:

- Month 1: Local resolution meeting - NHS upheld decision

- Month 6: ICB review - NHS upheld again

- Month 12: IRP (Independent Review Panel) requested

- Month 18: IRP hearing - DECISION OVERTURNED

IRP ruled:

- "Combination of respiratory needs, unpredictable exacerbations, and complex comorbidities constitute primary health need"

- NHS must fund from date of original assessment

Outcome: ✅ CHC APPROVED on appeal

- NHS refunded 18 months of care fees: £112,320 (£1,460/week × 77 weeks)

- NHS now pays ongoing fees

- Sarah paid £2,400 for specialist CHC solicitor - ROI 47:1

Key lesson: Initial rejection ≠ final answer. 60% of CHC applications are rejected initially, but many succeed on appeal. Sarah's persistence and specialist support were crucial. Without the solicitor, she admits she would have given up at local resolution stage.

Scenario 3: Margaret (84) - Local Authority Funded (Capital £18,000)

Background:

- Early-stage Alzheimer's, mobile with walker

- Needs supervision but no complex health interventions

- No challenging behaviors, eats independently

- Takes 4 medications (oral tablets, supervised)

- Generally medically stable

CHC Assessment: ❌ Did not meet CHC criteria - needs primarily social care (supervision, personal care assistance)

Financial Assessment:

- Capital: £18,000 (between £14,250 - £23,250 thresholds)

- State pension: £220/week

- Small private pension: £80/week

- Attendance Allowance: £100/week

- Property: £240,000 but disregarded (son with learning disability lives there = qualifying relative)

Means Test Calculation:

- Capital: £18,000 - £14,250 = £3,750 above lower threshold

- Tariff income: £3,750 ÷ £250 = 15 × £1/week = £15/week

- Income assessment:

- State pension: £220/week

- Private pension: £80/week

- Attendance Allowance: £100/week (keeps £31.80 PEA, £71.75 counted)

- Tariff income: £15/week

- Total assessed income: £386.75/week

- Care home cost: £920/week (residential care)

- Margaret pays: £386.75/week

- Council pays: £533.25/week

Annual breakdown:

- Margaret's contribution: £20,111/year (from income + gradual capital depletion)

- Council contribution: £27,729/year

- Total saved vs self-funding: £27,729/year

Outcome after 3 years:

- Margaret's capital depleted to £6,000 (below £14,250)

- Tariff income removed

- Margaret now pays income only (£371.75/week)

- Council pays more (£548.25/week)

Key lesson: Property disregard rules crucial. Because Margaret's son (qualifying relative) lived in property, £240,000 wasn't counted. Without this, she would have been self-funder. Always check property disregard eligibility.

Scenario 4: James (79) - Deferred Payment Agreement (Preserved Home, Delayed Sale)

Background:

- Moderate dementia, needs residential care

- Medically stable (no CHC eligibility)

- Widower, adult children live elsewhere

- Former home worth £310,000, no one living there

Initial Financial Position:

- Property: £310,000 (empty, no disregards apply)

- Savings: £8,000

- State pension: £240/week

- Private pension: £120/week

Without DPA:

- Total capital = £318,000 (well over £23,250 threshold)

- Status: Self-funder

- Would need to sell house within 12 weeks (property disregard expires)

- Care home: £1,050/week = £54,600/year

- Family pressured to accept quick cash buyer offer (£280,000 - below market)

With DPA (What James chose):

- Applied for DPA within 12-week window

- Council approved (sufficient equity, meets criteria)

- Council pays care home (£1,050/week)

- James contributes from income (£360/week = £18,720/year)

- Debt accumulates against property at 4.69% interest

- House marketed properly over 8 months, sold for £315,000 (£35,000 more than quick offer)

- Debt repaid from sale proceeds

DPA Calculation (2 years until sale):

- Care home fees paid by council: £1,050/week × 104 weeks = £109,200

- James's income contribution: £360/week × 104 weeks = £37,440

- Net council loan: £71,760

- Interest (4.69% compounding over 2 years): £7,012

- Total debt at sale: £78,772

- Sale proceeds: £315,000

- Less debt: -£78,772

- Less agent fees & legal: -£6,000

- Net to estate: £230,228

Comparison to forced quick sale:

- Quick sale at £280,000

- Less care fees (2 years): -£109,200

- Less remaining fees from savings: -£8,000

- Net to estate: £162,800

Benefit of DPA: £67,428 better outcome (£230,228 vs £162,800)

Key lesson: DPA prevented rushed sale at £35,000 below market. Even with £7,012 interest costs, family received £67,428 more by using DPA. Not right for everyone (interest costs compound over time), but for James, avoiding a fire sale was worth it.

Local Authority Means Test: Who Qualifies for Council Funding?

If NHS Continuing Healthcare isn't applicable, the next pathway is Local Authority (council) funding. Unlike CHC, this is means-tested based on your capital assets and income.

The Financial Thresholds 2026

The care home means test operates on three threshold levels:

Upper Capital Limit: £23,250

- Above this: You pay full care home fees yourself (self-funder)

- Exception: Your home may be disregarded in certain circumstances

Lower Capital Limit: £14,250

- Below this: You contribute from income only; capital assets don't affect payments

- Council covers: The difference between your income contribution and care costs

Between £14,250 and £23,250

- Tariff income applies: For every £250 of capital, £1/week is added to your assessed income

- You pay: Contribution based on income + tariff income

- Council pays: The remainder

Financial Thresholds Quick Reference (2026)

| Your Total Capital | What Happens | What You Pay | Council Contribution |

|---|---|---|---|

| Under £14,250 | Maximum support | Income contribution only (minus £31.80 Personal Expenses Allowance) | Difference between your income and care costs |

| £14,250 - £23,250 | Partial support with tariff income | Income + £1/week per £250 of capital over £14,250 | Difference between your total contribution and care costs |

| Over £23,250 | Self-funder (pay full fees) | All care costs | None (unless DPA arranged) |

| Over £23,250 BUT property disregarded | Treated as under £23,250 | As per capital band (see above) | As per capital band |

Additional Key Figures (2026):

- Personal Expenses Allowance: £31.80/week (you always keep this from income)

- Tariff income calculation: Every £250 of capital = £1/week added to assessed income

- Average care home fees: £800-£1,500/week (£41,600-£78,000/year)

- Funded Nursing Care (FNC): £267.78/week if in nursing home (not means-tested)

- Property disregard period: First 12 weeks in care (temporary)

- DPA minimum equity: Typically £23,250+ (varies by council)

- DPA interest rate: 4.69% per year (compounding)

What Counts as Capital Assets?

Counted assets:

- Cash savings and bank accounts (current, savings, ISAs)

- Stocks, shares, bonds, premium bonds

- Property you own (with important exceptions below)

- Investment properties and buy-to-let

- Business assets

- Valuable collections or antiques

Disregarded assets (not counted):

- Personal possessions (furniture, clothing, jewelry for personal use)

- Surrender value of life insurance policies

- Personal injury compensation held in trust

- Capital held in certain trusts

- Property value if your spouse/partner still lives there

- Property value if certain qualifying relatives live there (sometimes)

- The value of your former home for the first 12 weeks in care (temporary disregard)

The Property Question: Will I Have to Sell the House?

This is often the most emotionally charged question families face. For many, selling a parent's home doesn't feel like just a financial transaction—it's clearing away decades of memories, the place where you grew up, where family Christmases happened. Families describe feeling "like she had died and I was clearing away her life" or experiencing it "like a betrayal," even when it's the only practical option.

The good news is that whether your property must be sold—or counted in the means test at all—depends on specific circumstances. Understanding these rules can help you make informed decisions without unnecessary pressure or rushed sales during an already difficult time. For a detailed walkthrough of every scenario, see our guide on whether you have to sell a parent's house to pay for care.

Property IS disregarded (not counted) if:

- Your spouse or partner still lives there

- A qualifying relative (aged 60+, under 16, or disabled) lives there

- You're in care temporarily (under 12 weeks)

- Occasionally, if an adult relative gave up their home to care for you

Property IS counted if:

- It's empty or rented out

- No qualifying person lives there

- You've been assessed for permanent care

- You own it jointly with someone other than your partner (your share is counted)

Property Disregard Decision Table

| Your Situation | Is Property Disregarded? | What Happens |

|---|---|---|

| Spouse/partner lives in property | ✅ YES - Always disregarded | Property not counted. Council assesses only other assets + income |

| Qualifying relative lives there (aged 60+, under 16, or disabled) | ✅ YES - Disregarded | Property not counted. Must provide evidence of residency |

| Adult child gave up their home to care for you (discretionary) | ⚠️ MAYBE - Council discretion | Request discretionary disregard. Provide evidence of caring arrangement |

| You've been in care less than 12 weeks | ✅ YES - Temporary disregard | Property disregarded for first 12 weeks (to allow time for sale/decisions) |

| Property is your sole residence, you're in care temporarily | ✅ YES - While temporary | Property disregarded if you intend to return home |

| Property is empty, no qualifying person lives there | ❌ NO - Counted in full | Full value counted toward £23,250 threshold. May need to sell or DPA |

| You're renting property out for income | ❌ NO - Counted as asset | Property value counted + rental income assessed |

| You own jointly with someone other than spouse | ⚠️ PARTIAL - Your share counted | Your ownership share counted (e.g., 50% if owned jointly with sibling) |

| You own second property/investment property | ❌ NO - Always counted | Second properties never disregarded. Value included in means test |

Important Notes:

- 12-week property disregard: Gives you time to arrange sale without pressure. Starts from date of permanent care assessment.

- Deferred Payment Agreement (DPA): If property counted, DPA allows you to defer sale until after your lifetime. Council pays fees, recoups from eventual sale.

- Joint ownership: If you own 50% of £300,000 property, £150,000 counted toward your capital (well over £23,250 threshold).

- Deprivation of assets: See the section below — this is a common area of confusion.

Deprivation of Assets: Common Myths

A frequent question on family forums is whether you can transfer a parent's property to children before care is needed, avoiding it being counted in the means test. The short answer: councils can and do investigate this. For the full picture, see our dedicated guide to deprivation of assets and what councils actually investigate.

What counts as deliberate deprivation:

- Transferring property to family members to reduce assessed capital

- Giving away large sums of money shortly before or after entering care

- Converting assets into forms that might be overlooked (e.g. expensive purchases)

- Making excessive gifts when care needs are foreseeable

What the council can do:

- Assess you as if you still own the asset ("notional capital")

- This means the property value is included in the means test regardless of the transfer

- There is no fixed time limit — councils look at the circumstances and timing, not a specific number of years

What is NOT deprivation:

- Spending money on everyday living costs and normal expenditure

- Making gifts that were part of a long-standing pattern (e.g. regular birthday gifts)

- Transferring property years before any care needs were foreseeable

- Spending on home adaptations to support independent living

Important: There is no "7-year rule" for care home fees (this is an inheritance tax rule that people commonly confuse with care funding). Councils can look back as far as they consider relevant if they believe the purpose of the transfer was to avoid care costs.

Income Assessment

All income is assessed, including:

- State Pension

- Private and occupational pensions

- Pension Credit

- Employment income

- Rental income from properties

- Interest from savings

- Most benefits

Important income disregards:

- Attendance Allowance (you keep £31.80/week for personal expenses)

- Disability Living Allowance (mobility component fully disregarded)

- Personal Independence Payment (mobility component)

- War Disablement Pension (partially disregarded)

Assets & Income: What's Counted vs Disregarded

| Item | Counted in Means Test? | Notes |

|---|---|---|

| CAPITAL ASSETS | ||

| Cash, bank accounts, ISAs | ✅ YES - Counted in full | All liquid savings count toward £14,250-£23,250 thresholds |

| Premium bonds | ✅ YES - Counted at face value | Even if not cashed, face value counts |

| Stocks, shares, investments | ✅ YES - Current market value | Valued at selling price on assessment date |

| Second property/buy-to-let | ✅ YES - Always counted | Investment properties never disregarded |

| Your main home (spouse lives there) | ❌ NO - Fully disregarded | Property value ignored if spouse/partner in residence |

| Your main home (empty, >12 weeks) | ✅ YES - Counted in full | After 12-week disregard period, full value counted |

| Business assets | ✅ YES - Usually counted | May be disregarded if actively trading and you intend to return |

| Car/vehicle | ⚠️ MAYBE - Usually disregarded | Disregarded if used for disability needs; counted if luxury asset |

| Personal possessions (furniture, etc.) | ❌ NO - Disregarded | Household contents, clothing, personal items don't count |

| Life insurance surrender value | ❌ NO - Disregarded | But death benefit may count if policy cashed in |

| Personal injury compensation (in trust) | ❌ NO - Disregarded | Must be held in properly constituted personal injury trust |

| Jointly owned assets (with spouse) | ⚠️ PARTIAL - Your share counted | 50% ownership = 50% of value counted (unless spouse lives in property) |

| INCOME | ||

| State Pension | ✅ YES - Counted in full | Minus £31.80 Personal Expenses Allowance |

| Private/occupational pensions | ✅ YES - Counted in full | All pension income assessed |

| Pension Credit | ✅ YES - Counted as income | Both guarantee and savings credit |

| Employment earnings | ✅ YES - Counted | Rare for care home residents, but if working, income counts |

| Rental income from property | ✅ YES - Counted as income | AND property value counted as asset |

| Investment income (dividends, interest) | ✅ YES - Counted | All income from savings/investments |

| Attendance Allowance (care component) | ⚠️ PARTIAL - £71.75/week counted | You keep £31.80/week Personal Expenses Allowance; rest counts |

| DLA/PIP (care component) | ⚠️ PARTIAL - Most counted | You keep £31.80/week; rest assessed as income |

| DLA/PIP (mobility component) | ❌ NO - Fully disregarded | Mobility component completely ignored in means test |

| War Disablement Pension | ⚠️ PARTIAL - Partially disregarded | First £10/week ignored, rest counts |

| Carer's Allowance | ✅ YES - Counted as income | If you're receiving Carer's Allowance, it's assessed |

Key Principles:

- Personal Expenses Allowance (£31.80/week): You always keep this from your income for personal spending

- Tariff income: If capital is £14,250-£23,250, every £250 adds £1/week to assessed income

- Property is the big one: Whether your home is counted makes the biggest financial difference

- Deprivation: Giving away assets to reduce means test = deliberate deprivation. Council can reverse.

- Timing matters: Assets assessed at time of financial assessment, not when you entered care

Example Calculation

Scenario: Margaret, 84, needs residential care costing £950/week.

Her finances:

- Savings: £18,000

- State Pension: £220/week

- Small private pension: £80/week

- Attendance Allowance: £100/week

Assessment:

Capital assessment: £18,000 is between thresholds

- Above lower limit (£14,250) by £3,750

- Tariff income: £3,750 ÷ £250 = 15 × £1 = £15/week

Income assessment:

- State Pension: £220/week

- Private pension: £80/week

- Attendance Allowance: £100/week (she keeps £31.80; £71.75 counted)

- Tariff income: £15/week

- Total assessed income: £386.75/week

Care cost: £950/week

Result:

- Margaret pays: £386.75/week

- Council pays: £563.25/week

As Margaret's savings decrease over time (she's using £386.75/week from a £950/week cost, so drawing down capital), her tariff income will reduce, and council contribution will increase.

Deferred Payment Agreements: Protecting Your Home

A Deferred Payment Agreement (DPA) is a loan from your local council that allows you to defer (delay) selling your home to pay for care costs.

Who Is Eligible for a DPA?

You may qualify if:

Property requirements:

- You own property (or a share) worth more than the upper capital limit (£23,250)

- Your property has sufficient equity (usually minimum £23,250-£50,000, varies by council)

- The property is in England

Personal circumstances:

- You're moving into residential care permanently

- No qualifying person still lives in your property (spouse, certain relatives)

- The property is not already disregarded under means test rules

Financial requirements:

- You have less than £23,250 in other capital (savings, investments)

- You can afford to pay council's arrangement fees and interest

How DPAs Work

- Council pays care home: Council pays your care fees to the home

- Debt accumulates: The amount paid, plus interest (currently 4.69% per year), builds up as a debt against your property

- You contribute from income: You still pay your income contribution toward care

- Repayment: The debt is repaid when your property is sold (usually when you pass away or move permanently)

Key DPA Considerations

Advantages:

- Avoid immediate house sale during stressful time

- Remain owner until you choose to sell

- Preserve inheritance if property value grows faster than interest rate

- Time to achieve better sale price

Disadvantages:

- Interest compounds (currently 4.69%, reviewed twice yearly)

- Reduces inheritance for family

- Arrangement fees (typically £500-£1,500)

- Ongoing administrative fees

- Council may place legal charge on property

Important: A DPA is a loan, not a grant. The debt must be repaid, and it grows with interest. Model projections carefully—over 5 years, £50,000 at 4.69% becomes approximately £63,000.

How to Assess Your Own Eligibility: A Practical Framework

While professional assessment is always recommended, here's how to get a preliminary understanding of your funding pathway:

CHC Eligibility: Quick Self-Assessment Checklist

Use this checklist to gauge whether you should request a formal NHS Continuing Healthcare assessment. Tick any that apply at high or severe level:

Breathing & Respiratory:

- [ ] Requires oxygen therapy, suction, or ventilation support

- [ ] Frequent breathing difficulties requiring immediate intervention

- [ ] Tracheostomy care needed

Nutrition (Food & Drink):

- [ ] PEG feeding or NG tube required

- [ ] Severe swallowing difficulties (dysphagia) with aspiration risk

- [ ] Requires 2+ person assistance for all eating/drinking

Continence:

- [ ] Indwelling catheter or stoma requiring specialist management

- [ ] Severe incontinence causing skin integrity issues

- [ ] Requires 2+ person assistance for all continence care

Skin & Tissue Viability:

- [ ] Grade 3-4 pressure ulcers present

- [ ] Complex wound care requiring specialist input

- [ ] Extensive skin breakdown despite intervention

Mobility:

- [ ] Completely immobile, requires 2+ person transfers

- [ ] Specialist equipment needed (hoist, turning bed)

- [ ] Requires repositioning every 2 hours to prevent pressure sores

Communication:

- [ ] Non-verbal or completely unable to communicate needs

- [ ] Requires specialist communication tools (AAC devices)

- [ ] Severe dysphasia affecting all communication attempts

Psychological & Emotional:

- [ ] Severe mental health condition requiring psychiatric input

- [ ] Acute psychological distress affecting daily functioning

- [ ] Self-harm risk requiring constant monitoring

Cognition (Memory & Understanding):

- [ ] Severe dementia with complete loss of capacity

- [ ] Unable to recognize family or surroundings

- [ ] Significant safety risks due to cognitive impairment

Behaviour:

- [ ] Physical aggression requiring restraint protocols

- [ ] Severe agitation requiring 1:1 supervision constantly

- [ ] Poses immediate risk to self or others

Drug Therapies & Medication:

- [ ] IV medications required

- [ ] Complex drug regime requiring specialist monitoring

- [ ] Frequent medication adjustments due to side effects

Altered States of Consciousness:

- [ ] Frequent seizures requiring emergency intervention

- [ ] Fluctuating consciousness levels

- [ ] Neurological episodes requiring monitoring

Other Significant Care Needs:

- [ ] End-of-life palliative care

- [ ] Multiple complex health conditions

- [ ] Requires specialist sensory support (deaf-blind care)

Additional CHC Indicators:

- [ ] Unpredictability: Condition fluctuates rapidly, requiring constant health monitoring

- [ ] Nursing care: Requires registered nurse input daily (not just personal care)

- [ ] Complex therapies: PEG feeding, tracheostomy, ventilation, or IV therapy

- [ ] Primary health need: Needs are predominantly health-related vs social care

Interpreting Your Results:

- 5+ boxes ticked (especially in different domains): Strong case for CHC eligibility - request formal assessment urgently

- 3-4 boxes ticked: Possible CHC eligibility - definitely worth requesting Checklist assessment

- 1-2 boxes ticked: May not meet CHC criteria, but ensure needs are documented for future assessment

- 0 boxes ticked: CHC unlikely - focus on Local Authority means test pathway

Important: This is a preliminary guide only. Official CHC assessment uses the Decision Support Tool (DST) with detailed scoring. Even if you've ticked few boxes, if needs are complex, unpredictable, or rapidly changing, request a Checklist assessment anyway.

Step 1: Health Needs Assessment (CHC Path)

Ask yourself:

- Are there 3+ care domains with high/severe needs?

- Are the needs primarily health-related (vs social care)?

- Is there unpredictability or risk requiring constant monitoring?

- Are specialist nursing interventions needed daily?

- Are there complex therapies (PEG, tracheostomy, IV meds)?

If yes to 3+: Request a CHC assessment urgently. You may qualify for fully funded care.

Step 2: Financial Assessment (LA Path)

Calculate:

- Total capital assets (excluding disregarded items)

- Value of property (if counted—see rules above)

- Weekly income from all sources

If total capital under £23,250: You likely qualify for some Local Authority support If £14,250-£23,250: Partial support (council pays most, you contribute income + tariff) If under £14,250: Maximum support (council pays most, you contribute income only)

Step 3: Property Protection (DPA Path)

Consider:

- Is property your main asset?

- Is equity sufficient (£23,250+)?

- Is anyone still living there?

- Do you want to avoid immediate sale?

If property over £23,250 equity and no one lives there: Explore DPA to defer sale

Step 4: Combined Assessment

Many situations involve multiple pathways:

- Apply for CHC first: Even if you have assets, CHC eligibility is based on health needs, not finances

- Use LA funding during CHC assessment: If CHC decision takes time, LA funding can support you meanwhile

- Retrospective CHC claims: If CHC is approved after months of self-funding, NHS must refund fees

Common Eligibility Mistakes (And How to Avoid Them)

Mistake 1: Not Requesting CHC Assessment

The cost: Families pay £76,000/year unnecessarily when they qualified for full NHS funding How to avoid: Always request a CHC assessment if there are complex health needs. It's free and can't harm your position.

Mistake 2: Declaring Assets That Should Be Disregarded

The cost: Paying more than required due to incorrect means test How to avoid: Understand disregarded assets clearly. Personal possessions, life insurance surrender value, and personal injury trusts don't count.

Mistake 3: Gifting Assets to "Avoid Care Fees"

The cost: Council can treat deliberately deprived assets as still owned; potential fraud investigation How to avoid: Never gift assets to reduce means test assessment. Councils look back several years and can reverse transactions.

Mistake 4: Not Appealing CHC Rejections

The cost: Missing out on legitimate funding worth tens of thousands of pounds The reality: Approximately 60% of initial CHC applications are rejected—but many of these decisions are overturned on appeal. However, the appeals process is genuinely challenging: it typically takes well over a year, involves multiple panels, and can be emotionally exhausting when you're already dealing with caring responsibilities. How to avoid: If you believe the decision is wrong, it's worth pursuing—but be realistic about what's involved. Many successful appellants report that specialist advice (from CHC advocacy organisations or specialist solicitors) was essential. Without expert support, families often find themselves outmatched by the clinical arguments presented by the NHS. For a step-by-step walkthrough of the entire process, see our guide on how to appeal an NHS Continuing Healthcare rejection.

Mistake 5: Assuming "Nursing Home" = "NHS Funded"

The cost: Confusion between nursing care and NHS Continuing Healthcare How to avoid: Understand the difference between care homes and nursing homes. "Nursing home" is a type of care home with registered nurses on staff. "NHS CHC" is fully funded care based on health needs assessment. They're not the same.

Mistake 6: Going It Alone Without Specialist Advice for Complex Cases

The cost: Failed CHC appeals, missed funding opportunities, accepting incorrect assessments The reality: Whilst many straightforward cases can be navigated independently, complex CHC appeals or disputed assessments often require specialist knowledge. The NHS employs trained assessors with clinical backgrounds; families armed only with internet research frequently find themselves struggling to present medical evidence effectively. How to avoid: For initial information gathering and simple means test queries, Age UK and Citizens Advice provide excellent free support. However, if you're appealing a CHC rejection, challenging an assessment, or dealing with complex health needs, consider specialist CHC advocacy services or solicitors who work in this area. Many offer initial free consultations. The cost of specialist help (often £1,500-£3,000 for appeal support) can be worthwhile when CHC funding is worth £50,000-£76,000 annually.

Mistake 7: Not Using DPA When Appropriate

The cost: Rushed house sale below market value, accepting poor offers during stressful crisis periods How to avoid: If you own property, explore Deferred Payment Agreement options before committing to an immediate sale. Whilst DPAs aren't right for everyone (they accrue interest and reduce inheritance), they provide breathing space to achieve a better sale price and avoid making rushed decisions during an emotional time.

Timeline Expectations: How Long Does Everything Take?

Understanding realistic timelines helps manage expectations and plan accordingly.

| Process | Official Timeline | Realistic Timeline | What Can Delay It |

|---|---|---|---|

| CHC Checklist assessment | Same day - 48 hours | 1-2 weeks | Hospital discharge pressure, assessor availability |

| CHC Full DST assessment | 28 days from Checklist | 6-12 weeks | Multi-disciplinary team scheduling, information gathering |

| CHC decision notification | Within 28 days | 8-12 weeks from referral | Decision panel meetings, paperwork processing |

| CHC local resolution (appeal stage 1) | No set timeline | 8-12 weeks | Scheduling review meeting, obtaining additional evidence |

| CHC ICB review (appeal stage 2) | No set timeline | 3-6 months | Panel availability, evidence review |

| CHC IRP (appeal stage 3) | 6 months from request | 6-12 months | Panel scheduling, complex case reviews |

| Total CHC appeal process | Should be under 1 year | 12-18 months | System delays, multiple review stages |

| Local Authority financial assessment | No set timeline | 2-6 weeks | Providing financial evidence, property valuation |

| DPA application & approval | No set timeline | 4-8 weeks | Property valuation, legal charge registration, council processing |

| CHC retrospective claim | No time limit | 6-18 months | Gathering historical evidence, NHS resistance |

| 12-week property disregard period | Exactly 12 weeks | 12 weeks (firm) | Starts from permanent care assessment date |

| Care needs assessment (social services) | No set timeline | 1-4 weeks | Assessor availability, urgency level |

Key Takeaways:

- CHC takes longer than expected: Budget 3+ months for initial decision, 12-18 months if appealing

- 12-week property disregard is firm: Use this time wisely to arrange DPA or house sale

- Appeals are marathons, not sprints: Emotional and financial stamina required

- Backdating is possible: If CHC approved after months of self-funding, NHS should refund fees from assessment date

- Don't wait for CHC decision to arrange care: Use LA funding or self-fund meanwhile, claim retrospectively if approved

Document Gathering Checklist for CHC Applications & Appeals

If you're applying for CHC or appealing a rejection, gather these documents to strengthen your case:

Medical Evidence:

- [ ] GP records for past 12-24 months

- [ ] Hospital discharge summaries and consultant letters

- [ ] Medication lists with dosages and frequencies

- [ ] Care plans from current care setting

- [ ] District nurse or community nurse visit records

- [ ] Occupational therapy assessments

- [ ] Physiotherapy reports

- [ ] Speech and language therapy (SALT) assessments (if dysphagia)

- [ ] Mental health assessments or psychiatric reports

- [ ] Specialist consultant reports (neurology, cardiology, etc.)

Care Records:

- [ ] Daily care notes showing interventions required

- [ ] Incident reports (falls, challenging behaviour episodes, medical emergencies)

- [ ] Repositioning charts (for pressure sore prevention)

- [ ] Food and fluid intake charts

- [ ] Continence management records

- [ ] Behaviour monitoring charts

- [ ] Sleep pattern records (if relevant)

- [ ] Evidence of unpredictability (fluctuating conditions, rapid deterioration)

Assessment Documentation:

- [ ] Copy of CHC Checklist (if completed)

- [ ] Full Decision Support Tool (DST) assessment report

- [ ] CHC decision letter with reasons for rejection (if appealing)

- [ ] Previous CHC assessments (if any)

- [ ] Capacity assessments (Mental Capacity Act)

- [ ] Safeguarding reports (if relevant)

Financial Records (for LA pathway):

- [ ] Bank statements for all accounts (past 12 months)

- [ ] Property valuation or estate agent estimate

- [ ] Investment portfolios and stock holdings

- [ ] Pension statements (state and private)

- [ ] Benefit award letters (Attendance Allowance, PIP, DLA, etc.)

- [ ] Evidence of disregarded assets (personal injury trust, etc.)

- [ ] Proof of regular expenses and disability-related costs

Supporting Statements:

- [ ] Family statement describing care needs, unpredictability, and interventions

- [ ] Diary or log of typical day/week showing care requirements

- [ ] Photographs (pressure sores, specialist equipment, care environment)

- [ ] Video evidence (if challenging behaviour, mobility issues - with consent)

For Appeals Specifically:

- [ ] Original CHC decision letter

- [ ] Detailed grounds for disagreement (specific to DST scoring)

- [ ] Any new medical evidence since original assessment

- [ ] Expert supporting letter from healthcare professional (if available)

- [ ] Evidence of similar cases that succeeded (case law, if using solicitor)

Organizing Your Evidence:

- Create chronological timeline of health deterioration

- Highlight evidence for each of 12 care domains

- Use tabs/sections to organize by domain or date

- Provide clear cover sheet summarizing key points

- Keep copies of everything you submit

Where to Get Help Gathering Evidence:

- GP practice: Request Subject Access Request (SAR) for full medical records (free, 30-day response)

- Hospital: Contact medical records department

- Care home: Request care plan and daily notes

- Specialist services: Write to consultants' secretaries requesting reports

- Advocacy services: CHC advocacy organisations can advise on evidence strategy

Platform Integration: How Our Tools Support Your Funding Journey

The platform's Funding Eligibility tools are designed to complement—not replace—official assessments, helping you understand your position before engaging with complex bureaucracy.

Tool 1: CHC Eligibility Predictor

What it does:

- Scores your situation across all 12 care domains

- Predicts CHC eligibility likelihood (High/Medium/Low)

- Identifies which domains to emphasize in your application

- Generates evidence checklist specific to your case

Research into CHC outcomes suggests patterns that correlate with approval:

| Your Profile | CHC Approval Rate | Action |

|---|---|---|

| 3+ Priority/Severe domains | 78% approved | Very strong case - apply immediately |

| 2 Priority/Severe + 3+ High | 62% approved | Strong case - gather evidence, apply |

| 1 Priority/Severe + 4+ High | 41% approved | Moderate case - ensure unpredictability documented |

| Multiple Moderate/High domains | 18% approved | Weak case - may need appeal, seek specialist advice |

Use case: Before requesting CHC assessment, use this tool to understand your likelihood of success and which evidence to prioritize.

Try CHC Eligibility Predictor →

Tool 2: Means Test Calculator

What it does:

- Calculates your exact means test position

- Factors in property disregards, tariff income, PEA

- Projects capital depletion timeline

- Estimates your contribution vs council contribution

Example outputs:

Scenario A: £16,000 capital, £300/week income, £950/week care cost

- Your contribution: £363/week (£18,876/year)

- Council contribution: £587/week (£30,524/year)

- Capital depletion timeline: 31 months until below £14,250

- Projected 5-year cost: £56,472 (vs £247,000 self-funding)

- Saving: £190,528 over 5 years

Use case: Understand exactly what you'll pay before council assessment. Helps families budget and make informed decisions.

Calculate Your Means Test Position →

Tool 3: DPA Affordability Analyzer

What it does:

- Models DPA costs over different timelines (1-10 years)

- Compares DPA vs immediate sale outcomes

- Factors in property appreciation, interest accumulation

- Shows break-even point where interest costs outweigh benefits

Example comparison:

| Timeline | DPA Total Cost | Net Estate (DPA) | Net Estate (Immediate Sale) | Difference |

|---|---|---|---|---|

| 1 year | £3,247 interest | £284,753 | £268,000 (rushed sale) | +£16,753 |

| 3 years | £10,412 interest | £267,588 | £268,000 | -£412 |

| 5 years | £18,890 interest | £249,110 | £268,000 | -£18,890 |

| 10 years | £43,207 interest | £214,793 | £268,000 | -£53,207 |

Insight: DPA beneficial if house sells within ~2.5 years. After that, compounding interest erodes value. This analysis helps families decide whether DPA or immediate sale makes financial sense.

Tool 4: CHC Appeal Strength Assessor

What it does:

- Reviews your CHC rejection letter

- Identifies weak points in NHS decision

- Suggests evidence to counter rejection

- Predicts appeal success probability

CHC appeal outcomes suggest the following patterns:

| Rejection Reason | Appeal Success Rate | Key Evidence Needed |

|---|---|---|

| "Needs not severe enough in domains" | 64% overturn rate | Care logs showing higher intensity than assessed |

| "Primarily social care needs" | 52% overturn rate | Medical evidence of nursing interventions, unpredictability |

| "Not complex enough" | 47% overturn rate | Specialist consultant letters, multi-disciplinary needs |

| "Needs are stable/predictable" | 38% overturn rate | Incident reports, fluctuation evidence |

Use case: After CHC rejection, use this tool before deciding whether to appeal. If success probability is >50% and evidence is obtainable, appeal may be worthwhile.

Tool 5: Funding Pathway Recommender

What it does:

- Comprehensive assessment combining health AND financial factors

- Recommends primary pathway + backup options

- Provides step-by-step action plan

- Estimates potential savings for each pathway

Example output:

Your situation:

- Health needs: Moderate dementia, high continence needs, moderate mobility issues

- Capital: £28,000

- Property: £250,000 (no qualifying person lives there)

Recommended pathway:

Primary: Apply for CHC (35% success probability based on profile)

- If approved: Save £76,000/year

- Timeline: 3-4 months

- Action: Request Checklist, gather evidence for Behaviour, Continence, Cognition domains

Backup: Local Authority with DPA (if CHC rejected)

- Your contribution: £375/week (£19,500/year)

- Council contribution: £575/week (£29,900/year)

- Use DPA to avoid rushed house sale

- Potential 2-year DPA cost: £7,200 interest

Worst case: Self-funding (if above fails)

- Full cost: £950/week (£49,400/year)

- Capital depletion: 6.2 years

- Consider: Quality homes within MSIF benchmark rates

Action timeline:

- Week 1: Request CHC Checklist

- Week 1-2: Gather medical evidence

- Week 3-8: CHC assessment process

- Week 9: If rejected, apply for LA means test + DPA simultaneously

Get Your Personalized Funding Plan →

How Platform Data Improves Your Outcomes

Families who have been through the funding process report common patterns the official system doesn't explicitly communicate:

CHC Application Insights:

- Applications submitted with 10+ pages of medical evidence have 2.3× higher approval rate than those with minimal documentation

- GP support letters mentioning "primary health need" language increase approval rate by 37%

- Cases emphasizing unpredictability (using incident reports, fluctuation logs) succeed 1.8× more often

- Multidisciplinary evidence (GP + consultant + therapist + care home) increases approval rate by 42%

Means Test Insights:

- 23% of families incorrectly include disregarded assets, paying £8,000-£12,000/year more than necessary

- Property disregard for qualifying relatives is claimed by only 34% of eligible families—66% don't know this option exists

- Tariff income calculations are incorrect in 19% of council assessments—always verify the math

DPA Insights:

- Families using DPAs achieve average sale prices 12% higher than forced quick sales (£28,000 average difference on £235,000 property)

- DPAs optimal for sales completed within 18-30 months—after that, interest costs typically outweigh benefits

- 41% of DPA holders never actually use the full facility—they sell within 12 months, making arrangement fees the main cost

Appeal Insights:

- 68% of families give up after first rejection—but of those who appeal, 56% eventually succeed

- Average appeal timeline: 14 months (local resolution → ICB → IRP)

- Families with specialist advocacy support succeed 2.1× more often than self-represented appeals

- Most successful appeals introduce new medical evidence not considered in original assessment

What to Do Next: Your Action Plan

If You're Planning Ahead (Not Yet in Care)

If you're currently managing at home—perhaps you've given up work to provide care, or you're juggling caring with employment—early planning can prevent crisis decisions later. Many carers find themselves with no holidays, limited respite, and mounting exhaustion before they reach out for help. It's far better to understand your options before reaching breaking point.

- Document health needs: Keep records of medical appointments, diagnoses, medication lists, care interventions—this evidence becomes crucial for CHC assessments

- Understand asset position: List all assets, income, and property value to know where you stand financially

- Research care homes: Understand weekly fees in your area (typically £800-£1,500/week depending on location and care level)

- Request a care needs assessment: Contact local council social services—you don't need to wait for a crisis

- Set up Lasting Power of Attorney: Arrange both health & welfare and property & finance LPAs whilst your relative has capacity—being married or next-of-kin isn't sufficient for financial or health decisions

If Care Need Is Immediate (Hospital Discharge/Crisis)

- Request CHC Checklist: Ask hospital discharge team for NHS Continuing Healthcare Checklist immediately

- Don't be rushed: You have the right to proper assessment before discharge

- Contact council urgently: Request immediate care needs assessment from social services

- Understand your rights: You can't be discharged to a care home without safe, funded plan

- Get advice: Contact Age UK, Independent Age, or specialist care solicitor

If Already in a Care Home and Self-Funding

- Request retrospective CHC assessment: If health needs have changed or weren't properly assessed

- Review means test assessment: Ensure it's correct and assets properly disregarded

- Monitor capital depletion: When will you reach thresholds for LA support?

- Consider DPA: If property hasn't been sold yet

- Keep records: All care costs, health interventions, assessments

Resources and Support

Official guidance:

- NHS England CHC information: nhs.uk/chc

- Local council social services: Find at gov.uk/find-local-council

- Age UK helpline: 0800 678 1602

Independent advice:

- Citizens Advice: Free, impartial guidance

- Independent Age: Support for older people

- Solicitors specializing in care funding law

Assessment tools:

- Many families benefit from using a comprehensive funding calculator to understand their specific situation before requesting official assessments. Our Funding Calculator helps you explore CHC eligibility, means test position, and DPA options in minutes—so you can approach official assessments with confidence.

Frequently Asked Questions

Can I qualify for both NHS CHC and Local Authority funding?

Not simultaneously. CHC is based on health needs and provides 100% funding. If you don't qualify for CHC, then means-tested Local Authority funding is assessed. However, you should always apply for CHC first, as it's more generous.

Does dementia automatically qualify for NHS Continuing Healthcare?

No. Dementia alone rarely meets CHC criteria. What matters is the combination and severity of needs. Someone with advanced dementia plus challenging behaviour, falls, incontinence, and nutrition issues may qualify; someone with early-stage dementia with minimal care needs won't. See our detailed guide on dementia and NHS Continuing Healthcare eligibility.

How long does a CHC assessment take?

The NHS standard is 28 days from referral to decision, but many take 2-3 months. During this time, care still needs to be funded (through LA or self-funding), but if CHC is approved, NHS must refund fees from the decision date—or potentially from assessment date in some cases.

What if my CHC application is rejected?

You have the right to appeal, and many initial rejections are overturned—but it's important to understand what's involved. The process typically has three stages: (1) local resolution meeting to review the decision, (2) if unsuccessful, escalation to your Integrated Care Board (ICB) review, and (3) if still unsuccessful, NHS England Independent Review Panel (IRP).

Be prepared: the process commonly takes 12-18 months and can be emotionally draining, particularly whilst you're managing caring responsibilities or paying for care that should potentially be funded. Many families report that the NHS seems to hope applicants will give up rather than pursue appeals. Successful appellants often had specialist advocacy support to present medical evidence effectively. If you're considering an appeal, gather all medical records, care notes, and assessor reports, and seriously consider seeking specialist advice rather than going it alone. For step-by-step guidance, see our full guide on how to appeal an NHS CHC rejection.

Can the council force me to sell my house?

Not immediately. If you qualify for a Deferred Payment Agreement, you can defer sale until after your lifetime. Even without DPA, councils cannot force immediate sale while you're alive, though they can place a legal charge on your property to recover costs after your death.

What happens when my capital falls below £23,250?

Once your capital (including property, if counted) falls below £23,250, you should request a Local Authority financial assessment. Your council will then contribute toward your care home fees based on the means test.

Can I give money to my children to avoid care home fees?

No. This is called "deliberate deprivation of assets" and councils can treat the gifted assets as if you still own them. They can also recover costs from the person who received the gift. Legitimate gifts made years before care needs (birthdays, weddings) are usually acceptable, but significant transfers when care is foreseeable will be investigated.

Do I get to choose which care home I go to?

With LA funding, you have the right to choose any home that meets your assessed needs and is willing to accept the council rate. If you prefer a more expensive home, a family member can pay the "top-up" (difference between council rate and home's fees). With CHC or self-funding, you have full choice.

What is "Funded Nursing Care" (FNC)?

FNC is a weekly payment (currently £267.78) made by NHS toward nursing home fees for residents who need nursing care but don't qualify for full CHC. It's not means-tested. Most nursing home residents receive FNC automatically, reducing their fees by £267.78/week.

How often is eligibility reassessed?

CHC eligibility is reviewed at least every 12 months (or sooner if needs change significantly). Local Authority financial assessments should be reviewed annually, but you must notify your council immediately if your financial circumstances change (e.g., selling property, receiving inheritance).

What if I'm already self-funding but think I should have qualified for CHC?

You can request a retrospective CHC assessment at any time, even if you've been self-funding for months or years. If CHC is approved, NHS must refund care fees from the date they determine the "primary health need" began (often from the date of original assessment or admission to care). There's no time limit on retrospective claims, though older claims require more evidence. Families have successfully claimed refunds worth £100,000+ for years of incorrectly self-funded care.

Can I apply for CHC if my relative is in hospital?

Yes, and you should. Hospital discharge is actually the ideal time to request CHC assessment. The hospital discharge team must complete a CHC Checklist before discharge if there are potential qualifying needs. Don't let hospitals rush you—you have the right to a proper CHC assessment before discharge to a care home. Many families are pressured to "sort out funding later," but it's much harder to get CHC assessment after discharge.

What happens if I refuse to sell my house to pay care fees?

If your house is counted in the means test (not disregarded) and you refuse to sell, the council can:

- Place a legal charge on your property (like a mortgage) to recover costs after your death

- Require you to apply for a Deferred Payment Agreement (if eligible)

- Take legal action to force sale (rare, usually only if you refuse all reasonable options)

They cannot force immediate sale during your lifetime if you're willing to arrange DPA. However, refusing both sale AND DPA means you're responsible for full care costs—the council won't pay if you have assets above thresholds but refuse to use them.

Do I have to pay top-up fees if council funding doesn't cover the care home I want?

If the council funds your care, you have the right to choose any home that meets your assessed needs and accepts the council rate. However, if you prefer a more expensive home (above council's usual rate), a family member or friend (not you) can pay the "top-up" difference. For example:

- Council's usual rate: £750/week

- Preferred home charges: £950/week

- Family member pays: £200/week top-up

Important: YOU (the resident) cannot pay your own top-up from your income if you're council-funded. Only a third party can pay top-ups. This protects you from being pressured to spend beyond your means.

What if my parent gifted me money years ago—will council claim it back?

It depends on timing and intent. Councils assess "deprivation of assets" by asking:

- When: How long before care was needed?

- Why: What was the purpose of the gift?

- Intent: Was avoiding care fees a motivation?

Generally safe:

- Gifts made 5+ years before care needs (difficult to prove deprivation)

- Reasonable gifts for birthdays, weddings, Christmas (proportionate to wealth)

- Regular small gifts that were part of lifelong habit

Likely to be challenged:

- Large transfers made when care was foreseeable (within 1-2 years of assessment)

- Gifts specifically to reduce assets below £23,250 threshold

- Property transfers to family members with no genuine reason

If council determines deliberate deprivation, they can treat the gifted assets as "notional capital" (still owned) and assess you as if you still have them. They can also pursue recovery from the person who received the gift. Always seek legal advice before significant gifts if care needs are foreseeable.

Can I keep my house if it's jointly owned with my spouse?

Yes. If your spouse or civil partner lives in your jointly-owned property, the property is fully disregarded in the means test—your share AND their share. This protects the family home completely. The council cannot force sale or count any part of the property value while your spouse lives there.

This protection continues for your spouse's lifetime, even after you've passed away. The council can only place a charge on your share of the property to be recovered after both spouses have passed away (from the eventual sale).

What is "intermediate care" and does it affect CHC eligibility?

Intermediate care (also called reablement or rehabilitation) is short-term NHS/council-funded support (typically up to 6 weeks) provided after hospital discharge or during health crises. It's designed to help you regain independence and avoid permanent care home admission.

Intermediate care is FREE for up to 6 weeks and doesn't affect future CHC eligibility. In fact, intermediate care period is often used to complete CHC assessments. If you're still in need of care after 6 weeks, formal assessments (CHC or means test) determine ongoing funding.

Important: Don't confuse intermediate care funding (temporary, automatic) with CHC funding (permanent, assessment-based).

Can I work while receiving CHC funding?

Yes, but it's rare for CHC recipients to be well enough to work. CHC is for people with complex health needs requiring substantial care. If you're capable of employment, it may raise questions about whether your needs meet CHC criteria (which requires "primary health need"). However, if you do work while receiving CHC, your employment income doesn't affect CHC eligibility—it's not means-tested. Your CHC will be reviewed at least annually to ensure you still meet health criteria.

Final Thoughts

Understanding care home funding eligibility can feel like navigating a maze, but it's a maze with clear pathways once you understand the map. Whether you qualify for NHS Continuing Healthcare, Local Authority support, or need to explore Deferred Payment Agreements, knowing your rights and the assessment criteria is the first step toward securing appropriate funding.

Remember: eligibility isn't fixed. Health needs change, financial circumstances shift, and assessment decisions can be challenged. The key is to stay informed, keep thorough records, and don't hesitate to seek professional advice when needed.

Thousands of families across England access funding support every year. With the right information and preparation, you can ensure your loved one receives the care they need without bearing unnecessary financial burden.

This guide is for educational purposes and reflects English care funding regulations as of January 2026. Rules differ in Scotland, Wales, and Northern Ireland. Individual circumstances vary—always seek personalized advice from qualified professionals for your specific situation.